The Hunger Beneath the Numbers

The Hunger Beneath the Numbers

Why the U.S. TMS market is the hungriest it has ever been — and who is actually buying.

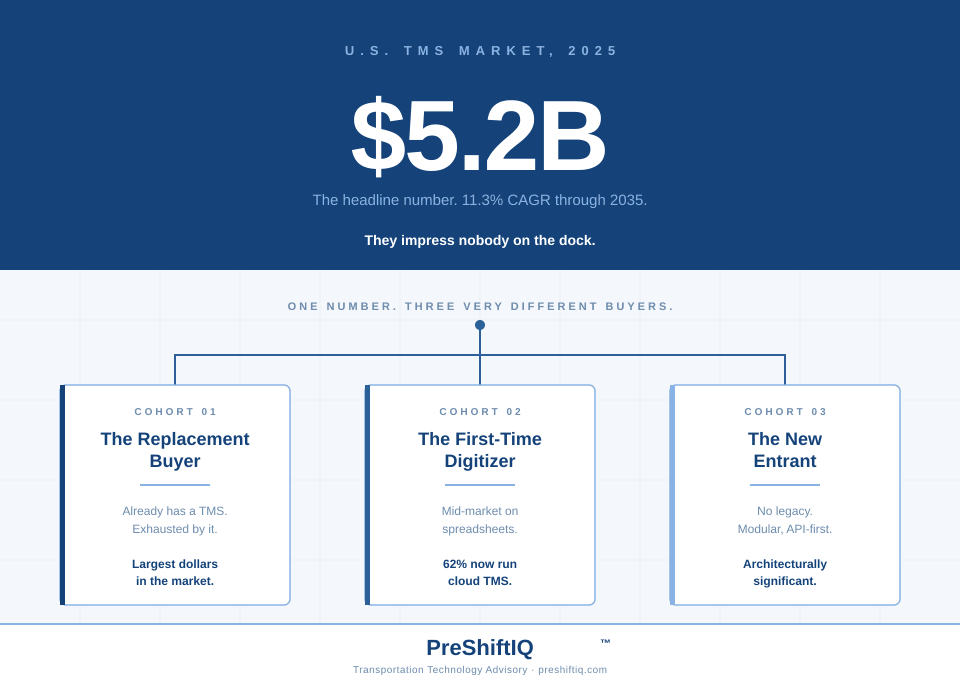

$5.2 billion.

That is the U.S. transportation management system market in 2025. By 2035 it more than doubles to $12.3 billion. An 11.3% compound annual growth rate, every year, for a decade.

Numbers like that get quoted in board decks and pitch presentations. They impress investors. They impress nobody on the dock.

The interesting question is not how big the market is. The interesting question is who is actually buying — and why now.

Three Buyer Cohorts. Three Very Different Motivations.

Strip away the marketing copy and U.S. TMS demand resolves into three distinct buyer profiles. Each is moving for different reasons. Each is buying a different kind of solution.

Cohort 1 — The Replacement Buyer

Already has a TMS. Bought it five to ten years ago. Probably enterprise. Probably on-premise. Probably tethered to an ERP that has not been touched since the original implementation.

This buyer is not new to transportation technology. They are exhausted by it.

Their TMS works. Sort of. The contracts auto-renew. The vendor support tickets get answered. But the system has aged — visibility gaps, manual workarounds the team built around platform limitations, integrations that connect but do not actually work, and a UI that no new hire wants to learn.

“The replacement buyer is not asking 'do I need a TMS?' They are asking 'do I need this TMS?' That is a very different conversation, and the answer is increasingly no”.

These buyers represent the largest dollar opportunity in the market. They also have the longest sales cycles, the deepest procurement scrutiny, and the highest switching cost. Vendors who try to land enterprise replacement deals without a serious case-study portfolio lose. Vendors who do it well build $1M+ ARR relationships.

Cohort 2 — The First-Time Digitizer

Mid-market shipper or 3PL. Spreadsheets, email, phone calls, paper bills of lading. Maybe a homegrown Access database from 2009 that one administrative employee maintains.

This buyer is finally doing it — moving operations onto real software for the first time. The decision is not driven by a competitive analysis. It is driven by a board mandate, a private equity sponsor, an insurance audit, an FDA traceability requirement, or a customer who has stopped accepting paper.

First-time digitizers are the fastest-growing segment in U.S. TMS adoption. 62% of mid-sized shippers now deploy cloud-based TMS — up sharply from a few years ago. The constraint is no longer awareness. It is execution.

This cohort buys differently. They are not running RFPs against five enterprise vendors. They are looking at three to five mid-market platforms, asking three or four operator-friendly questions, and signing in 90 days. Time-to-value matters more than feature parity. The vendor that wins is the vendor whose implementation team can stand up the system without breaking the operation that was already running on spreadsheets.

Cohort 3 — The New Entrant

Startup shipper, broker, 3PL, or asset-based carrier launching with technology in the room from day one. No legacy. No contracts to break. No staff to retrain because there is no staff yet.

This buyer is small in dollar terms. They are also the most architecturally significant cohort in the market. They are the proof point for what TMS can be when nothing else is in the way.

New entrants choose modular, API-first, cloud-native platforms with embedded financial tooling, native carrier identity verification, and modern UI. They are not constrained by legacy. They will pay subscription fees that scale with usage. They will switch vendors quickly when something better appears.

New entrants also expose the gap between what mature TMS vendors actually deliver and what greenfield buyers actually need. When a Cohort 1 enterprise replacement evaluates the same platforms a Cohort 3 startup loves, the enterprise often passes — too modular, too unfamiliar, too far from their procurement comfort zone. That gap is where the next decade of competitive shake-out happens.

The Survival Question

Behind every cohort is a quieter question that nobody wants to ask out loud: what happens to operators who do not adopt?

The data is not pretty. Mid-market operators running on spreadsheets carry 3% to 8% excess freight spend versus peers running modern TMS. On a $50M freight network that is $1.5M to $4M of avoidable cost every year. Compounded over five years, $7.5M to $20M. That is not a software decision. That is a survival decision.

Insurance carriers are tightening underwriting standards on shippers without electronic traceability. Major retail customers will not onboard new suppliers without API-based shipment data. FDA traceability requirements under FSMA Section 204 are now in force for food categories. The cost of not adopting transportation technology has stopped being theoretical.

"The market is not growing because vendors are good at selling. It is growing because not adopting has become the more expensive choice."

What the Headline TAM Hides

The $5.2 billion U.S. TMS figure is real. The 11.3% CAGR is real. But the headline number obscures the fact that the U.S. market is actually three different markets, growing at three different speeds, for three different reasons.

Enterprise replacement is a slow, deep, high-dollar market driven by exhaustion with legacy. Mid-market first-time digitization is a fast, broad, medium-dollar market driven by external pressure. Startup adoption is a small but architecturally significant market that previews where the next decade goes.

Vendors who treat the TMS market as one homogeneous opportunity miss two of the three cohorts. Buyers who use the headline numbers as their evaluation framework end up with platforms built for a different cohort than theirs.

What This Means for the Buyer

Before evaluating any TMS — before sitting through a single demo — the buyer should answer one question. Which cohort am I? Replacement, first-time, or new entrant?

The right vendor for a Cohort 1 enterprise replacement is almost never the right vendor for a Cohort 2 first-time digitizer. The procurement framework, the implementation methodology, the support model, the pricing structure, and the partnership ecosystem are all different. A vendor optimized for one cohort frequently fails the other.

Most buyers do not realize this until twelve months into a misaligned implementation. PreShiftIQ has audited those projects. The pattern repeats.

But Hunger Doesn't Guarantee Good Outcomes

The market is moving. Buyers are moving. Vendors are racing to keep up — and the dominant marketing motion of 2025 and 2026 is the same one we saw in 2018 and 2019, just with a new label slapped on the front of every product page.

AI.

Every vendor has it now. Every demo features it. Every RFP gets a slide deck claiming intelligent this, predictive that, autonomous the other thing. Buyers — across all three cohorts — are being sold AI as the answer.

Most buyers do not actually know what they are being sold. The next paper takes that apart.

Sources: Precedence Research (Feb 2026), Global Market Insights (Dec 2025), MarketsandMarkets, Mordor Intelligence, Fortune Business Insights, A2Z Market Research, FactMR. PreShiftIQ vendor audit data and engagement findings.